India’s smartphone market shipments declined 4.1% year-on-year in Q1 2026, dropping to 31.0 million units, according to IDC’s Worldwide Quarterly Mobile Phone Tracker. If you thought cheaper was always an option in the world’s most price-sensitive smartphone market, think again. The Indian smartphone market decline in Q1 2026 tells a story of rising costs, shrinking choices at the budget end, and a consumer base quietly being nudged upmarket, whether they like it or not.

The twist? Despite fewer phones being shipped, the market actually grew 5.8% in value terms. The average selling price hit a record $302, up 10.4% year-on-year. So yes, Indians bought fewer smartphones, but spent more on each one. That is either a sign of a maturing market or a market where budget buyers simply ran out of affordable options. Spoiler: It is a bit of both.

In This Article

Why Did India’s Smartphone Market Decline in Q1 2026?

The culprit is not difficult to identify. Global memory price inflation drove up component costs across the board, forcing brands to either hike device prices or quietly exit low-margin segments. With reduced promotional activity after the festive season and little room for aggressive discounting, demand remained soft. Channel inventory was front-loaded ahead of anticipated price increases, but actual consumer absorption lagged behind supply movement.

Aditya Rampal, Senior Research Analyst at IDC Asia Pacific, noted that, unlike previous market cycles, brands have significantly pulled back on discounting because rising input costs constrained their ability to stimulate demand. Brands are now leaning on product differentiation and EMI-driven financing models rather than flash sales.

Read Also: iPhone and Android Can Now Text Each Other Privately Thanks to iOS 26.5

The Entry-Level Collapse Is the Headline Nobody Wanted

The most dramatic number in this report sits at the budget end of the market. The sub-$100 smartphone segment declined a staggering 59% year-on-year, with its market share crashing from 18% to just 8%. This is not a dip. This is a near-disappearance.

Rising memory costs made it economically unviable for brands to continue offering affordable sub-$100 devices at scale. With fewer options available, budget-conscious consumers were not really choosing to upgrade. They were being pushed upward by necessity, not aspiration.

Mid-Range Fills the Gap, Premium Quietly Thrives

As entry-level demand cratered, the $100 to $200 segment stepped up as the market’s primary volume driver, growing 10% year-on-year and capturing a 45% share of total shipments.

Higher price bands also performed well. The $400 to $600 range grew 29% year-on-year, the $600 to $800 segment expanded 32%, and the $800-plus tier held steady at a 7% share. Premium smartphone demand in India remained resilient, supported by financing options and a consumer segment that has largely been insulated from memory-driven pricing stress.

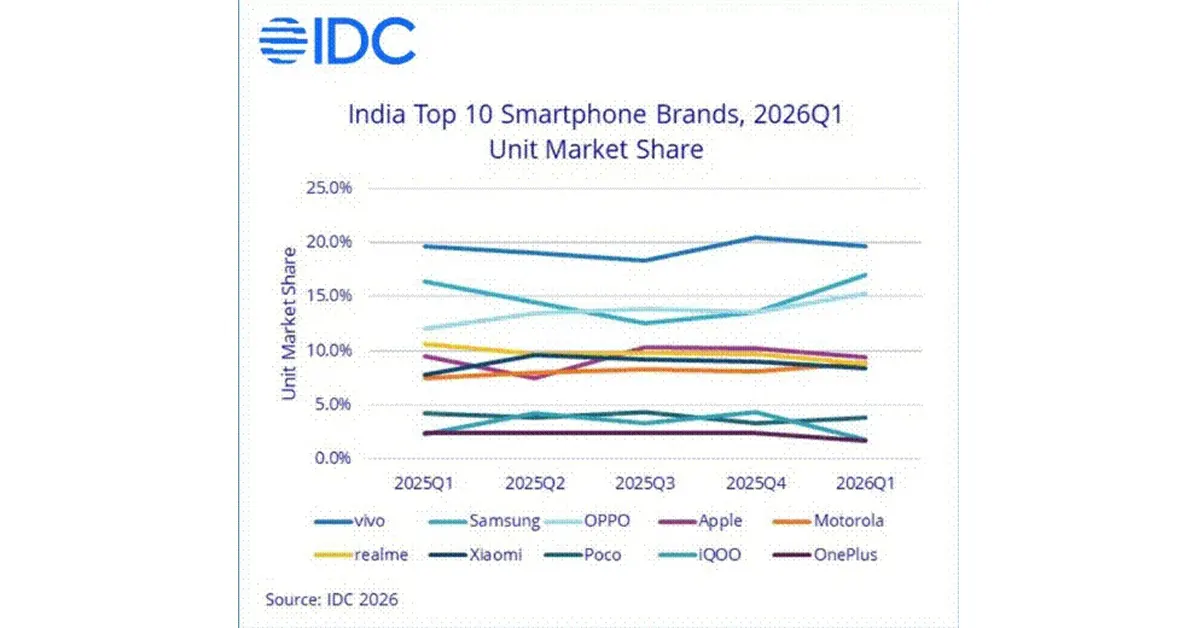

Brand Rankings: Familiar Faces, One Surprise

The top five brands in India for Q1 2026 were vivo (No. 1), Samsung (No. 2), OPPO (No. 3), Apple (No. 4), and Motorola (No. 5). Motorola’s entry into the top five is notable and reflects smart positioning in the mid-range segment.

Apple, despite a slight dip in shipments, retained a dominant 28% value share of the entire market. The iPhone 17 alone accounted for roughly 4% of total smartphone volumes in India. That single model outselling entire brand portfolios is a remarkable statistic.

Offline Retail Makes a Comeback

Online channels, which thrived on discount-led demand, took a visible hit. Online shipments fell 14% year-on-year, with online’s share dropping from 42% to 38%. Offline retail gained ground, rising from 58% to 62% share, as brands leaned on physical stores to manage pricing pressure and drive assisted purchase behaviour. When consumers need financing and hand-holding through a more expensive purchase decision, the physical store becomes relevant again.

What Happens Next: Memory Prices, Festive Hopes, and a Cautious Outlook

IDC’s outlook for the first half of 2026 is cautiously stable, buoyed by existing inventory buffers. However, annual shipment forecasts are being revised downward as memory inflation shows no sign of easing.

Upasana Joshi, Senior Research Manager at IDC Asia/Pacific, delivered a pointed observation. Indian consumers have traditionally delayed purchases in anticipation of festive discounts. However, with the global memory shortage expected to continue into 2027 and rupee depreciation adding cost pressure, prices are only likely to go higher. Consumers who are considering an upgrade may find better value in buying sooner rather than waiting for deals that may not materialise at the same scale they once did.

Recovery in the second half of 2026 will hinge on pricing stability, festive season demand, and whether brands can develop financing models that make higher-priced devices accessible to the mass market.

Read Also: Samsung Galaxy M and F Series Get Big Price Cuts in India Starting May 8

The Bigger Picture

India’s smartphone market is clearly undergoing a structural transformation. This is not just a bad quarter. The collapse of affordable sub-$100 smartphones, the record average selling price, and the growing dependence on EMI models point to a market that is quietly repricing itself out of reach for millions of first-time and budget buyers. That is a real problem for a country where volume has always been the engine of growth. Premium is thriving, mid-range is holding, but the bottom of the pyramid is crumbling. If that gap is not addressed with smarter financing models and cost innovation, the world’s most exciting smartphone market risks becoming a tale of two very unequal halves.

{kind=link}